Is the wealth effect just that - a temporary effect?

Is the wealth effect just that - a temporary effect?

Things always happen faster nowadays? Not necessarily so. In 1720, John Law’s Compagnie des Indes, better known as the Mississippi company, blew up in spectacular fashion just a few years into an experiment in breaking the link between money and precious metals, taking France’s national finances with it.

In 2022, the ‘everything bubble’ in bonds, equities and real estate which appear to be in the process of popping have been some twenty years or more in the making. Yet there are distinct similarities between the events in France in the early eighteenth century and what is going on now in financial markets, and the causes are familiar ones: low interest rates, money printing and then inflation.

The Mississippi company story is very much of the super-nova sort. Law opened a bank in Paris in 1715, acquired interests in a number of French overseas trading posts the following year (hence the Mississippi moniker), then took over the French national debt, refinancing it at a lower interest rate before offering to exchange its obligations for Mississippi company stock at a discount (a classic debt-for-equity swap).

In 1719 he started to print paper money (the livre tournois), and Mississippi company stock sky-rocketed as more equity was issued on margin using paper-money loans. Cue bubble, then instability (a fall in the value of French money on the international markets), then bust. Attempts to support company stock failed, and it ended up falling 90% in value. Law fled France in ignominy, although his ideas of printing money to buy up debt to keep interest rates low are eerily similar to central-bank monetary policy post 2008…

The Mississippi bubble period spawned the term ‘millionaire’ from the easy profits made by the company’s early stock-holders. It also saw the first use of the term realize, as in realising profits, the process of turning ‘ideal property into something real’.1

The last twenty years or so have seen an extraordinary increase in financial wealth as the price of bonds, equities and real estate have all risen together. The emergence of inflation in 2021, and the central-bank response to this problem in the form of aggressive interest-rate hikes, has called this trend into question in the most spectacular fashion, judging by how asset prices have faired in 2022. It is this process of re-evaluating the nature of financial wealth which raises the question about the durability of the wealth effect, and also how one realizes one’s wealth in the light of inflation and central banks’ ongoing response to it.

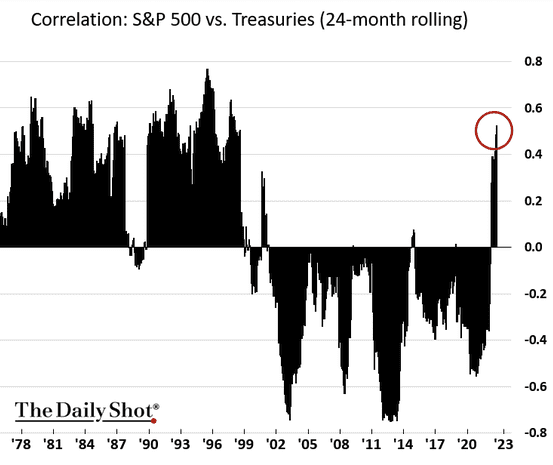

The graph below illustrates the wealth-effect problem clearly. For much of the past two decades or more, bonds have been negatively-correlated to equities. A classic 60/40 equity/debt pension portfolio made money from equities in the good times, but also money from bonds during the bad times as central banks aggressively cut rates in recessions only to raise them slowly in the recovery (true in the US after the 2000-1 and 2008-9 recessions). Tame inflation never demanded sharp central-bank responses. Bonds and equities were negatively-correlated, hurrah for the 60/40 portfolio. Then came inflation, and bond-equity correlation went positive, crushing asset values everywhere.

The wealth effect therefore starts to look like a temporary phenomenon in which falling rates and falling inflation help elevate asset prices - directly on bonds, indirectly on equities (as the present value of discounted cashflows that underpin equity valuation rise), and directly on property (borrowing more at a lower interest rate).

The argument for the temporary nature of this wealth effect is strengthened when one looks at the historic drivers of lower rates and lower inflation, something one can do in the way John Law did in terms of printing money to buy debt to lower rates.

One can look at the graph above and link the timing of the correlation shift to key events in Asia - the end of the Asian financial crisis in the late 1990s and the admission of China into the World Trade Organisation (WTO) in 2001, events which saw huge buying of US Treasuries throughout Asia as countries suppressed their foreign-exchange levels with the dollar and bought up dollar-denominated debt to strengthen their currency reserves.2

Debt levels in the developed world rose sharply as a result of the cost of debt falling due to Asian buying. After 2008, this debt-driven cycle was abetted by central banks both by keeping policy rates low and also by indirectly encouraging financial risk-taking through limiting the supply and yield on government debt through quantitative easing (QE).

Globalisation, measured in terms of global trade volumes, peaked in 2007. Foreign reserve accumulation peaked in 2014, and the process of de-globalisation from a geopolitical point of view arguably had its first major catalyst with Trump’s China tariffs in 2019. With the confiscation of Russia’s foreign reserves earlier this year following the invasion of Ukraine, the role of dollar reserves (in the form of US Treasuries) appears to be changing, and taken together, it seems these forces of de-globalisation, both in monetary and geopolitical terms, are not about to change direction.

From an investor’s point of view, the disinflationary effect of cheap labour and cheap goods (from globalisation) which has propelled the wealth effect is now going in reverse. Add in the effect of 2020 and 2021’s huge Covid-related fiscal stimulus and supply-chain disruptions, as well as energy-price inflation from serial under-investment in the natural-resources sector and the effect of sanctions on Russia, and suddenly central banks are having to start hiking interest rates aggressively to fight inflation.

The problem may be that if these trends (de-globalisation, energy shortages, rising labour costs and geopolitical instability) prove enduring, then it is possible that inflation doesn’t return to 2% or lower, save for the unpalatable proposition of a deflationary financial collapse. If inflation stabilises in the mid-single digits, then interest rates will likely reflect this, and the wealth effect that has been such a boon for investors will face long-term headwinds.

The hysteria in the UK press in the last week in some ways reflects this unfortunate realisation. Setting aside the anti-Tory and anti-Brexit ranting, there was genuine alarm about the safety of people’s pensions and the value of housing. Unlike the US where mortgages are fixed for 30 years, the UK’s mortgage market is either floating or comprised of 2 to 5 year fixed rates, and is thus highly sensitive to interest-rate changes.

The prospect of a UK mortgage costing 6% as opposed to 2% at a time when households are already struggling with higher energy and food bills is not only an immediate problem but a long-term one from the perspective of the overall level of house prices and a possible reversal of their long-term trend higher, population increases notwithstanding. People may well have to wake up to the truth spoken by Warren Buffet that interest rates are the gravity of asset prices.

Whether investing in the stock market, the bond market or buying a house, living in a higher-rate environment will mean a new set of choices in terms of both outlook and asset allocation. Using the UK as an example, the idea that house prices only go up has been gospel for decades. The negative equity trap of the early 1990s and the blip in house prices during the global financial crisis are distant memories. This may be about to change.

If the wealth effect does prove to be a passing one and we are coming to the end of the everything bubble, then investors face two related problems. First, like the newly-minted millionaires of the Mississippi bubble era, is the question of how to realize profits. This is especially true of illiquid investments; real-estate funds are already starting to be gated to halt redemptions. In any case, if everyone sells at the same time, you get a crash. The second is what to do next - in a world where almost everything seems to be financialised or leveraged to some degree or another, including the money system itself (as we found out from the UK gilt market last week), what actually remains real and not ideal?

Edward Chancellor, The Price of Money, Allen Lane, 2022, p50 and p55

Russell Napier, The Asian Financial Crisis 1995-98, Harriman House, 2021, pp360-1