Government bond markets shouldn't be interesting, but they are getting that way.

Government bond markets shouldn't be interesting, but they are getting that way.

Sadly we live in an age when financial markets are increasingly dominated by central banks and the pronouncements of the luminaries who run them. Mr Kuroda, outgoing governor of the Bank of Japan (BoJ), had an oratory high-point in 2015 when he started channelling Peter Pan with reference to the Japanese central bank’s bold new bond-buying programme.

“I trust that many of you are familiar with the story of Peter Pan, in which it says, 'The moment you doubt whether you can fly, you cease forever to be able to do it. Yes, what we need is a positive attitude and conviction.”

One thing that doesn’t seem to be flying too well right now is the BoJ’s yield-curve control programme. Until December 2022, the central bank used open-market operations to keep the yield on 10yr Japanese government bonds (JGB’s) within 0.25% above or below the zero bound (0%). Unique among the developed-world central banks in 2022, the BoJ had stubbornly and heroically kept interest rates unchanged as inflation rose and its central-banking peers raised rates in response.

Then on the 20th December, the BoJ shocked markets (shocked I say) by keeping rates unchanged but increasing the band of its yield target from 0.25% to 0.50%. Governor Kuroda shrugged off the change, saying, "This is neither a tightening nor a step toward an exit. This is a tweak to the monetary policy operation,"1

With an overnight central-bank policy rate still in negative territory (at -0.1%) but with Japanese CPI inflation at 3.7% in December 2022 and the producer price index (PPI) for the same month coming in at 10.2%, it looked in many ways as though the BoJ was in fact bowing to inflationary (and peer) pressure.

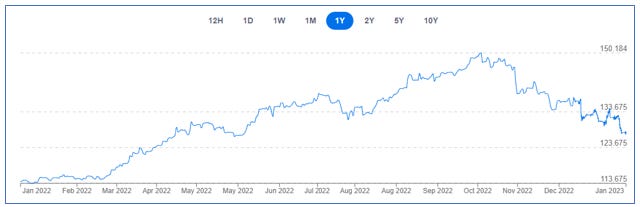

The yield on 10yr JGB bonds promptly rose to levels near the new 0.5% limit and with higher yields, the yen strengthened from 137 against the dollar to its current level of around 128 at the time of writing. This is quite some turn around given the BoJ was rumoured to have intervened in the currency markets on at least two occasions in previous months to defend the yen as it slid to 150. Perhaps this yen rally was just the effect of higher yields in Japan, or perhaps it was really a dollar weakness ‘thing’ as the Fed comes close to the end of its hiking cycle. Perhaps the yen strength has been flow driven (the selling of foreign reserves or US Treasury bonds to purchase JGB’s, whether by the BoJ or commercial banks in Japan). It could be a combination of all of these factors.

Yet all isn’t quite right with the BoJ’s policy. Last week, the new 0.5% yield limit on the 10y bond was being heavily and repeatedly tested, with the BoJ forced to execute massive amounts of quantitative easing (QE) in order to keep the peg in place. The figures are huge (think March 2020 Covid-intervention huge), with approximately $78b of JGB’s purchased on Thursday and Friday alone2. The BoJ has again intervened heavily on Monday 16th ahead of its scheduled two-day policy meeting on Tuesday and Wednesday. The market smells blood.

With the yield-curve control policy under severe pressure and with QE being strained to the limit, will the BoJ be forced to change tack? Opinion is mixed, but there seems to be three options in play: first, a further widening of the band, perhaps to 0.75%; secondly, per Citibank, that the system of yield-curve controls could be abandoned entirely; or thirdly, that the BoJ does nothing and sticks to its guns3.

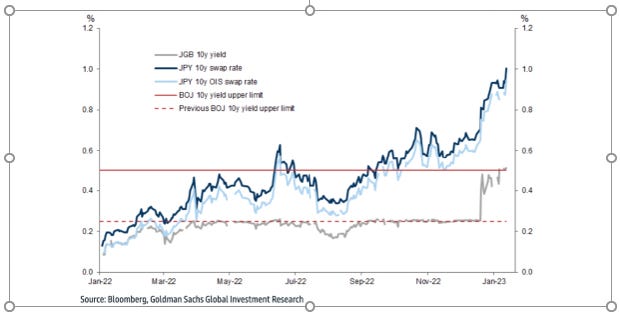

Each option has its own consequences, but the market is clear about what it thinks is going to happen. The graph below shows the 10yr JGB yield in grey at just below 0.5% while the 10yr JPY swap rate (not subject to BoJ intervention or control) in blue at a considerably higher level of around 1%. The market is clearly pricing much higher yields in Japan, and this may be another part of the explanation of the recent strength of the yen against the dollar.

Even with the market speaking loudly, we must await the BoJ’s policy decision over the coming days. The problem as ever though is, in a world of fully-flexible credit-backed money, that credibility is all. When central banks are forced by markets to change directions, odd and dramatic things can happen.

The world of currencies has an impossible trinity: one cannot have a stable currency, a sovereign monetary policy and an open capital account all at the same time. One of the three must be sacrificed. Either the currency must float on world markets, the currency must be pegged to something else (the dollar for example), or restrictions must be placed on capital flows in but especially out of the country. This was America’s problem during the Bretton Woods era, China’s current problem (it has a largely closed capital account), and it yet may prove to be Japan’s problem in the coming months and quarters.

If the BoJ were to abandon yield-curve control, one would expect yields to rise sharply across the curve (per the Goldman graph above). As of Q3 2022, Japan’s public debt-to-GDP was a mere 266%, so clearly rising yields could cause solvency worries in short order. While Japan has a strong capital position abroad, one would expect pressure to repatriate funds to support the domestic economy (and the yen), which in turn would force yields on foreign government bonds higher as well as depressing other asset markets (credit and equity). At the very least, one would expect a sharp rise in market volatility in the short term as a new normal was tested out.

For now at least, the BoJ is printing money to defend the bond market. But the impossible trinity suggests that a sovereign monetary policy comes at the price of one’s currency on the foreign exchanges (one can control the amount of money, or the price of it, but not both), and the repatriation of foreign-based capital back to Japan notwithstanding, one might assume the yen will start to weaken if the BoJ has to keep on doing QE at this crazy pace. If it stops yield-curve control and yields rise, one ought to expect a knock-on effect of rising yields elsewhere, with all the negative effects that has on other asset prices such as equities.

In the very short term though, it may be that the BoJ’s QE largesse is helping markets - global stock markets, especially the racier tech growth elements, have had a great start to the year, and assets like bitcoin are looking perky once again. Massive printing means more liquidity, and we all know that means buy the dip and the rally with reckless abandon.

Yet behind all this is a sense that while governments and central banks have managed to get away with a lack of fiscal discipline and monetary orthodoxy for nearly a decade and a half now, the return of inflation and supply-disruptions (from lockdowns, de-globalisation, the energy transition and other long-term factors) after a long absence has changed the game. With the new risk of inflation expectations becoming de-anchored, the policy options of the past (print and cut rates) aren’t available in the same way or with the same likely outcome. When one is talking about massive government bond markets (Japan 266% of GDP, US 120% of GDP and so on), the stakes are clearly very high. Interesting times indeed.

Mitsuru Obe, BOJ shocks market with surprise widening of yield curve band, Nikkei Asia, 20/12/2022.

Toshihiro Sato and Ryo Saeki, BOJ’s record-breaking $78b bond buying fails to halt rising yields, Nikkei Asia, 14/01/2023.

Leo Lewis and Kana Inagaki, Bond traders set to test BoJ ahead of key policy decision, Financial Times, 16/01/2023