Crowding out - the problem that links the debt ceiling, rate hikes and bank woes.

Crowding out - the problem that links the debt ceiling, rate hikes and bank woes.

In East Germany (the old German Democratic Republic), there were two regions which were unable to pick up TV and radio signals from West Germany (the old German Federal Republic). Broadcasters in the west were mindful of the propaganda effect of portraying the capitalist lifestyle to their communist neighbours so used powerful broadcast antennae to make sure die Ossis were fully aware of the wonders and plenty that they were missing out on.

The hapless inhabitants of these two areas (in the south around Dresden and east of Rostock in the north) were known disparagingly by their fellow East Germans as being the ‘valley of the clueless’. With the White House refusing to engage with Congress on the debt ceiling and with the Federal Reserve still hanging tough on interest-rate hikes in the face of multiple bank failures, it sometimes feels as though Washington is in some signal dead-zone where news from the outside world isn’t being received.

It hasn’t just been a bad week for long-term predictions, but for very short-term ones as well. On Sunday, Jamie Dimon, CEO of JP Morgan (ticker JPM) and new owner of the assets of First Republic Bank (FRC), said the banking crisis was over. On Wednesday, during the post-FOMC press conference, Fed Chair Jay Powell also said the banking system was strong. Minutes later, shares of PacWest Bancorp (PACW) tanked in the after-market as the company said it was considering options including a sale. Other bank stocks have tumbled as well this week.

There is a difference between stupidity and ignorance, but it would be deeply unfair to accuse either Mr Dimon, as head of the largest bank in the US, or Mr Powell, chair of the most important financial institution in the world, of either. In times of crisis, those in charge always say things are ok - that is essentially their job. To admit the extent of the current problems, and then to admit that there is no easy solution, is just not what’s done in America. Every public figure in the US should recall President Jimmy Carter’s ‘malaise speech’ delivered on July 4th 1979 and how being downbeat (honest..) can ruin your reputation for good and all.

One ought not therefore to expect frankness from public figures at the present time. What is happening is an unravelling process or denouement caused by a long string of events and policy mistakes. In Greek tragedy, this event is called anagnorisis - the point at which the main character (in this case the US) finds out the true nature of their own circumstances. What makes this painful in America is that a domestic crisis is manifesting itself just at the point at which the country’s reach abroad - symbolised perhaps by wide questioning of the role of the US dollar - is diminishing too.

On Wednesday, the Fed Funds rate rose to 5.25%, and changes to the wording of the FOMC statement suggest this might be the end of the current hiking cycle. In 2021, while the Fed was still claiming inflation was transitory, not only were rates at zero but Chairman Powell was suggesting there would be no hikes until 2024 (‘not even thinking about thinking about hiking’). The market - investors, banks, everyone - acted accordingly, gorging on cheap money, much of it created by the Fed through quantitative easing (QE) as it monetised the huge Federal deficits resulting from the pandemic interventions.

Fast forward to 2023 and there is a banking crisis. Bought when yields were at historic lows, bank assets yield less than the current Fed Funds rates and less than the yield offered by US T-bills and money market funds. Caught offside by the rapid rate-hiking cycle, many smaller banks cannot offer higher yields to depositors so funds are leaving banks and heading elsewhere. The big national banks (JP Morgan et al) are also offering low deposit rates, but their too-big-to-fail status offers them an allure of safety. Bigger banks have seen deposit inflows, but with savers wising-up to better alternatives, this may not last - and this is where the crowding out problem might emerge.

The graph above shows the current interest costs for the US national debt. As of March 30th 2023, US debt to GDP was 120%, and with rates now north of 5% and with much of the national debt short-dated, the interest cost is soaring, and may reach $1.5b by year end depending on how much debt is issued. For context, US defence spending was $746b in 2022. So these high rates might be a tonic for inflation and may end the speculative mania in US financial markets, but Uncle Sam is also being crippled by them. But the government always gets funded - and the attractive rates being offered by short-dated US T-Bills has started to draw in savers even as the US debt ceiling approaches.

Back in March, Silicon Valley Bank (SVB) closed its doors as it was forced to sell assets on the cheap to meet depositor demands, and the fact their asset values had dropped so sharply (due entirely to the rapid rise in interest rates) meant their capital was insufficient, hence being forced into liquidation. While SVB was clearly badly run and its risk management was naive, its swollen balance sheet was in part a result not only of the 2020-1 Fed money-fest, but also of the 15 years or so of zero or near-zero interest rates which preceded it.

Warren Buffet describes interest rates as the gravity of asset prices. With rates at zero, malinvestment becomes rife, and this manifested itself in a tech boom which emphasised revenue growth over cashflow generation or even profitability, and which attracted huge fund flows into private equity and venture capital, hence the asset growth at banks like SVB.

While the Fed’s QE1 in December 2008 might have been justified to stabilise the mortgage market during the financial crisis, the subsequent bouts of QE, coupled with zero rates and a seeming willingness to accede to any and all market pressure to cut rates (the taper tantrum of 2013 and the pre-covid rate cuts and QE of 2019 stand out, but the super-charged QE of 2020-1 was clearly transformational) created what appeared to be an everything bubble. This bubble started to crack last year, led by the biggest growth area of all, government debt.

To think therefore that the banking crisis is the case of a few bad apples is clearly to miss the point of what’s happening now. Zero rates meant investors’ time horizons extended out way into the future, hence high valuations and sky-high asset prices as it seemed the good times could last forever. With the Fed’s rate hikes, that time horizon is imploding. It has started to affect the banks, and commercial real-estate is the key vector there, but the idea that other non-bank or shadow lenders (venture capital, private equity, insurers, pension funds) will escape is clearly wishful thinking, especially if the Fed keeps rates high as it says it will.

How does the US debt ceiling fit into all of this? Secretary for the Treasury Janet Yellen said last week that the Federal Government will run out of money at the beginning of June. Partial government shut-downs have happened before. There was one in 2013 which you might only have noticed if you were visiting New York and couldn’t go up the Statue of Liberty. The debt standoff in 2011 was a big one, involving as it did a downgrade to the US’ credit rating , but its resolution was taken as a positive by markets.

It’s probably best to assume that the debt ceiling will get raised at some point, especially if the White House engages with Congress and political concessions are made. If it doesn’t and the US defaults or goes down the cray-cray road of issuing $1 trillion platinum coins to plug the gap, then all bets are off anyhow.

If the debt ceiling is raised without limit, there is going to be a lot of debt issuance by the government. If it’s only raised for a year say, then there may be even more issuance as the Treasury seeks to create enough funds to ensure the government stays funded past the Presidential election in November next year. Federal tax yields in 2023 have been feeble, in part because of the absence of capital gains with a falling stock and bond market last year. With higher interest rates causing a spike in funding costs as discussed above, the US deficit is rising sharply, and it’ll rise further if there is a recession.

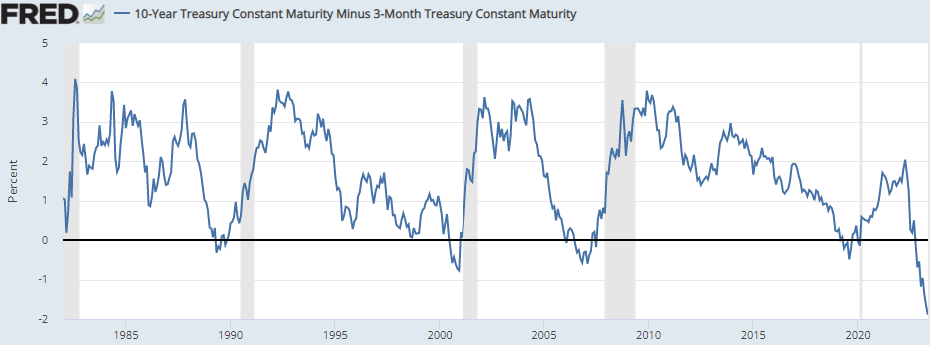

Like a black hole sucking in light, the funding needs of the US government may start to crowd out the rest of the economy. Banks are already losing the funding fight against money market funds and T-Bills, and corporates will likely struggle too - both in terms of having to offer a higher yield to finance their debt and in terms of bank lending being restricted as savings flow into the government bond market. Then there’s the yield curve, inverted due to Fed rate hikes. An inverted yield curve where short-term rates exceed longer-term ones is poison to bank lending since the banks’ job is essentially a duration swap - borrowing short and cheap and lending longer and at higher interest rates. At -1.89%, the 3-month / 10-year US rate is currently the most inverted it’s been since the 1980s (see graph above).

The Fed can offer some mitigation (cutting access to or the yield offered by the reverse repo facility for example), but it’s the double whammy of a high Fed Funds rate and the effect that has on interest payments and the US primary deficit that are the real killers for the private sector. In any case, restricting reverse repo is a form of financial easing, and the Fed is still ostensibly in tightening mode.

The US and its institutions are clearly walking a fine line, one between two unpalatable choices - crowding out the private sector to save the public sector and inducing deflation as a consequence, or to admit the mistakes of the last 15 years are too grave to be resolved, reversing the current monetary-policy stance, and giving-in to inflation.

The road taken will as ever be one driven by political considerations about time, especially with elections on the horizon in 2024. Short-term gain for long-term pain, or short-term pain for long-term gain. Especially in the light of government fiscal responsibility and how that affects the private sector of the economy, that is the moral conundrum that the debt ceiling really raises.

If you enjoyed this post please subscribe below to get future instalments sent direct to your inbox - so cheap it’s free!

Excellent piece Charlie. It seems central bankers and supranational bankers have all forgotten the crowing out advice from Hume, Smith and Hamilton. They will undoubtedly save the public sector, at least in the near term, at the risk of private capital. Deflation anyone?