Uncharted waters? The problems with financial forecasting in 2022.

Uncharted waters? The problems with financial forecasting in 2022.

'The value of your investments may fall as well as rise. Past performance is no guide to the future.’ Despite this advice being at the foot of every financial services advertisement in the UK, the finance industry and economics profession seems obsessed about predicting the future. At the start of 2021, consensus was for 2% inflation in the US last year and it turned out to be 7%. Now the market is pricing as many as 7 Fed rate hikes in 2022 when it was effectively pricing none as recently as September. Is it time to call Mystic Meg?

For those who aren’t regular readers of The Sun newspaper, Mystic Meg is their in-house astrologer. She shot to national fame in the mid-1990s when she became part of the Saturday-night national lottery TV show. History doesn’t however relate her success rate in identifying jackpot winners. It may not have been much worse than financial forecasters attempts to predict inflation last year.

Astrology aside, the problem with forecasting is not to what extent the future will be like the past, but how it will be different. There is a small and exclusive group of individuals who have excelled this. The philosopher Friedrich Nietzsche is one such person. With the decline of Christian morality in nineteenth century, he foresaw that the battles of the future would be ones between the ideologies trying to replace it, and in so doing, his thought foreshadowed the conflicts of the twentieth century (fascism vs bolshevism, capitalism vs communism). That’s fairly smart.

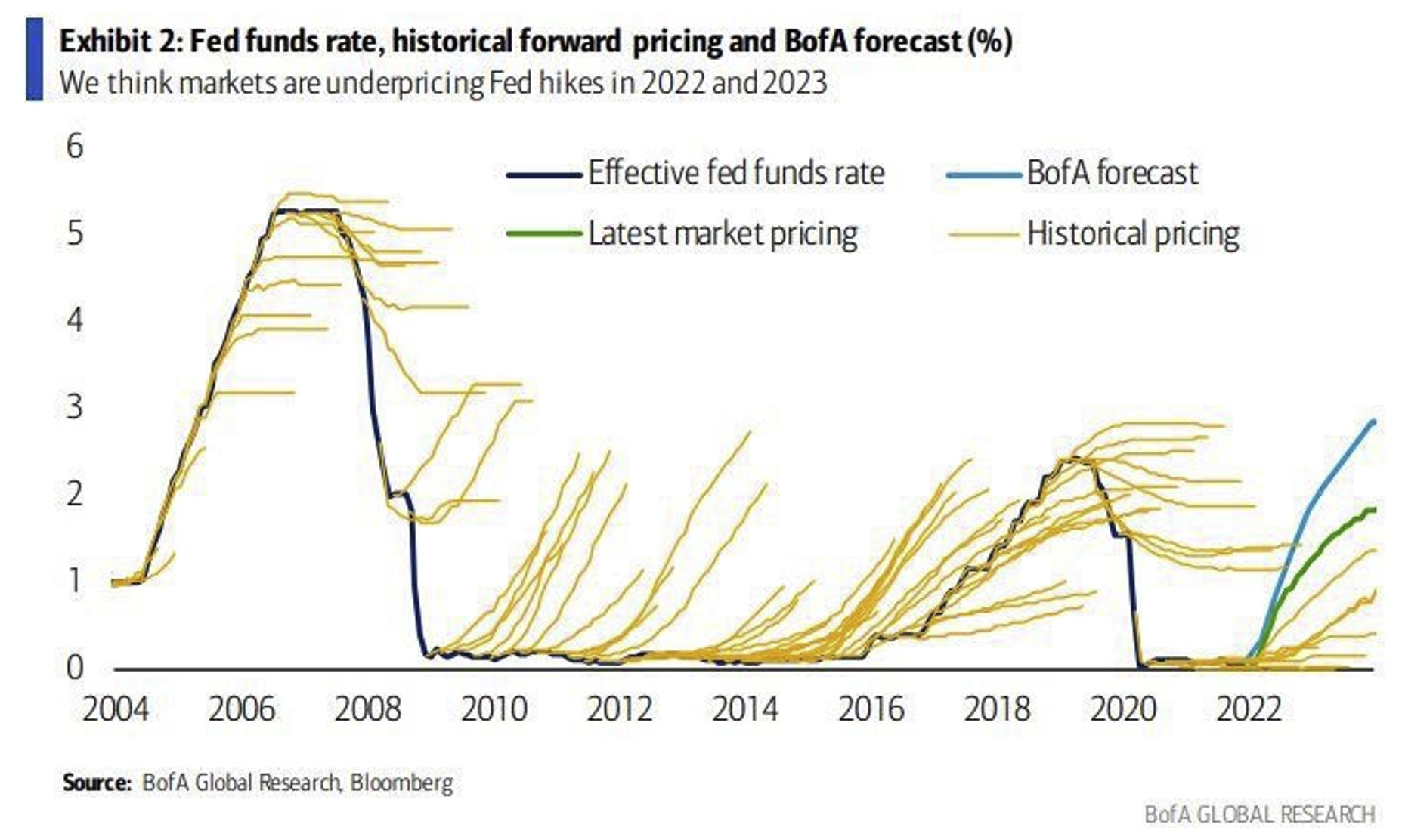

On a slightly more mundane level, forecasting interest rates and inflation are tasks where the difficulty lies in appreciating the effect of economic change in the face of both recent experience and the binding effect of economic doctrine. The graph below illustrates this problem perfectly. The black line shows the actual US Fed Funds interest rate, while the whispy-yellow lines show what path the market was pricing at various points. Clearly the predictive power of the market leaves much to be desired.

While this may suggest the bond market and its associated derivatives are no longer very good predictors of monetary policy and inflation, there are reasons still to take what the bond market says very seriously.

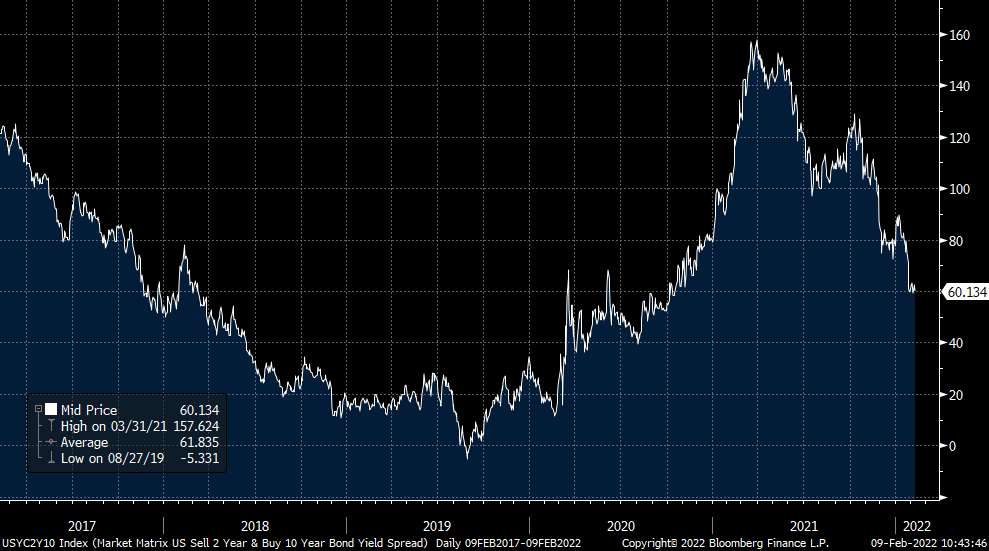

The US yield curve is currently flattening. The graph below shows the yield differential between the 2yr and 10yr US Treasuries. Currently it is at 0.6%, down from nearly 1.6% in 2020. An inversion (such as occurred in 2019) is often seen as a good indicator of an impending recession. The curve is flattening because of the hawkish tone of the Fed as well as suggestions the US economy is slowing (not least because there will be much less fiscal stimulus in 2022).

This curve flattening could be interpreted as meaning that with inflation still rampant and the market pricing Fed rate hikes up to 1.25% or so by year end, the scope of the Fed to do much more tightening beyond what is already priced without inverting the yield curve and causing a painful recession is limited. In the context of very strong inflation, this is clearly a major problem, and may reflect the fact that the Fed’s hands are ultimately tied. This causes a lot of confusion for the market and market commentators in terms of drawing on their experience and knowledge of the past to predict what is likely to happen in the next few years.

Economists and market participants often use history in a strange way. As the inflationary problem has emerged in the last year or so, there has been much chatter about which is the best analogue. Is it like the 1970s, the 1940s or even the 1910s? Is the current market volatility like Q4 2018 (Fed policy error) or Q1 2000 (dotcom crash)?

This approach reflects a very particular view of history, and one which has fallen out of favour since the Enlightenment in the middle of the eighteenth century. While the Enlightenment ushered in a belief in human progress to a brighter future through the use of science and reason, in many ways it replaced an older view of history where the stories of the past, particularly those of ancient Rome and Greece, were seen as direct guides to action in the present.

This approach was known as ‘history as the teacher of life’ (or historia magister vitae for those fond of Latin). For example when Napoleon pitched up in Egypt of all places in 1798, he was consciously mimicking the heroic exploits of Alexander the Great (356-323 BCE). Even Admiral Nelson’s destruction of the French fleet at the Battle of the Nile that year was interpreted as symbolic of Alexander burning his ships, preventing a retreat, and basically saying it’s Persia or broke.

While this might seem like a very oblique analogy to use with respect to investment and the financial markets in 2022, the point is that it raises the question of what the world will look like if central banks can’t deal with inflation, or whether their attempt to deal with it causes more problems than it fixes (this is particularly true of Europe where the government bond yields of countries like Italy are shooting higher in a dangerous manner). The recent past may not be a great guide in this instance.

Much of the investment wisdom of the past forty or so years has developed to the backdrop of falling inflation, expanding debt, globalisation, deregulation, capital mobility, and capital taking the lion’s share of earnings to the detriment of labour. All of this has been happening in the context of a fully-flexible credit system of money (aka the fiat system) which is itself a notable departure from the past. With so much change, the drawing of direct historical analogies has to be done with caution.

In terms of asset allocation, it is therefore worth asking far more serious questions about what happens if there is a discontinuity with the past because central banks can’t tame inflation or if they cause another financial crisis by their attempt to do so. This is particularly true in the context of the persistent strength in the commodity market in the face of growing central-bank hawkishness. It’s quite possible that the past won’t provide a simple answer to the question of what one should do next, or at least not one which the market can get behind in a straightforward manner.

Got this far and want more? Please click the link below to subscribe and receive Market Depth direct to your inbox.