The Federal Preserve - Jay is in a Jam.

The Federal Preserve - Jay is in a Jam.

So it turns out that unlike a light switch, the world economy cannot just be switched back on again with no consequences after a lockdown. In the US, despite the Fed’s transitory inflation narrative, October’s monthly headline Consumer Price Index (CPI) print was 0.9% (core inflation rose by 0.6%), with the annual increase now 6.2%. Immediately following the release on 10th October, and for the first time in a while, the price of gold spiked sharply as inflation came in higher than expected. All is not well.

On the surface, the immediate cause of this inflation spike has largely been attributed to supply-chain bottlenecks due to disruptions caused by the post-lockdown reopening. The backlog of goods at ports, higher commodity prices (note China’s October Producer Price index or PPI of 13.4% vs 12.4% estimate) as well as ongoing employee-hiring issues suggests that we’ll continue to see elevated levels of inflation into 2022. This scenario leads to two questions: first, will these issues resolve themselves, and secondly, if they don’t, what do central banks do in response?

The transitory narrative, supported by the economics of supply and demand, suggests that the cure for higher prices is higher prices. If wages, which are rising but arguably not as quickly as inflation, don’t keep pace with price rises, consumers reduce their spending. Demand falls, and with it prices. This is the classic supply shock which can cause a recession. If one looks at falling consumer sentiment in the US, particularly in relation to rising auto and housing costs, then this effect is starting to make itself felt. Add in the long-term trends in demography (the aging of the world’s population), technological advance and the effect of excessive levels of debt, then one can argue that the current inflationary trends won’t ultimately lead to an inflationary regime change. At some point, we’ll return to the disinflationary pre-Covid economic world.

There is certainly some truth in this. Much of the inflation in the US is on the goods rather than the service side, and this may rectify itself in time. Much of the last 30 years can be characterised by falling service prices in the US creating a disinflationary backdrop. This shift was however reliant on the outsourcing of manufacturing to countries with lower production costs, notably China. It’s at this point that the argument with respect to a new period of secular inflation starts to get some credence.

Globalisation, if measured by global trade, peaked in 2007 and has pretty much flatlined since. With Trump’s trade war starting in 2018, an event which clearly pre-dated Covid, it is arguable that a process of de-globalisation started. With the US rivalry with China showing no sign of abating during Joe Biden’s presidency, the urge to bring production home, which will entail higher costs especially through wages, looks set to continue. As a result, the world may be entering a new phase of resource nationalism, onshoring of supply chains, and possibly currency wars.

Alongside wages, the other chief cause of inflation is energy costs. Behind the argument of higher prices curing higher prices is a twofold demand/supply argument. Either higher prices reduce demand (absent wage increases), or more supply comes online at higher prices which then causes prices to fall. On the supply side of this argument, the problem with energy costs, which again pre-date Covid, is that the shift away from fossil fuels for environmental reasons was already reducing oil and gas exploration investment. The US shale boom proved an unprofitable but important marginal source of supply which kept energy costs down in the 2010s. This is unlikely to be repeated, especially given the political climate and investors shunning oil and gas companies due to ESG concerns. Energy supply looks far less flexible than it once did. The risk from higher commodity prices, in terms of energy but also food, is that this is what consumers notice the most, and could thus prove the principal cause of inflation expectations becoming de-anchored. This is the great central-bank fear.

The market is starting to price in rate hikes in the US in 2022, with Fed fund futures (which anticipate future Fed policy rates) implying a first hike by July next year. So far, the Fed has only had to state that it possesses the tools to fight inflation. Merely invoking the spirit of Paul Volcker, the legendary Fed Chairman who slew the inflation dragon of the 1970s, is all well and good, but the Fed may now be called upon to act, and this is where the problems start.

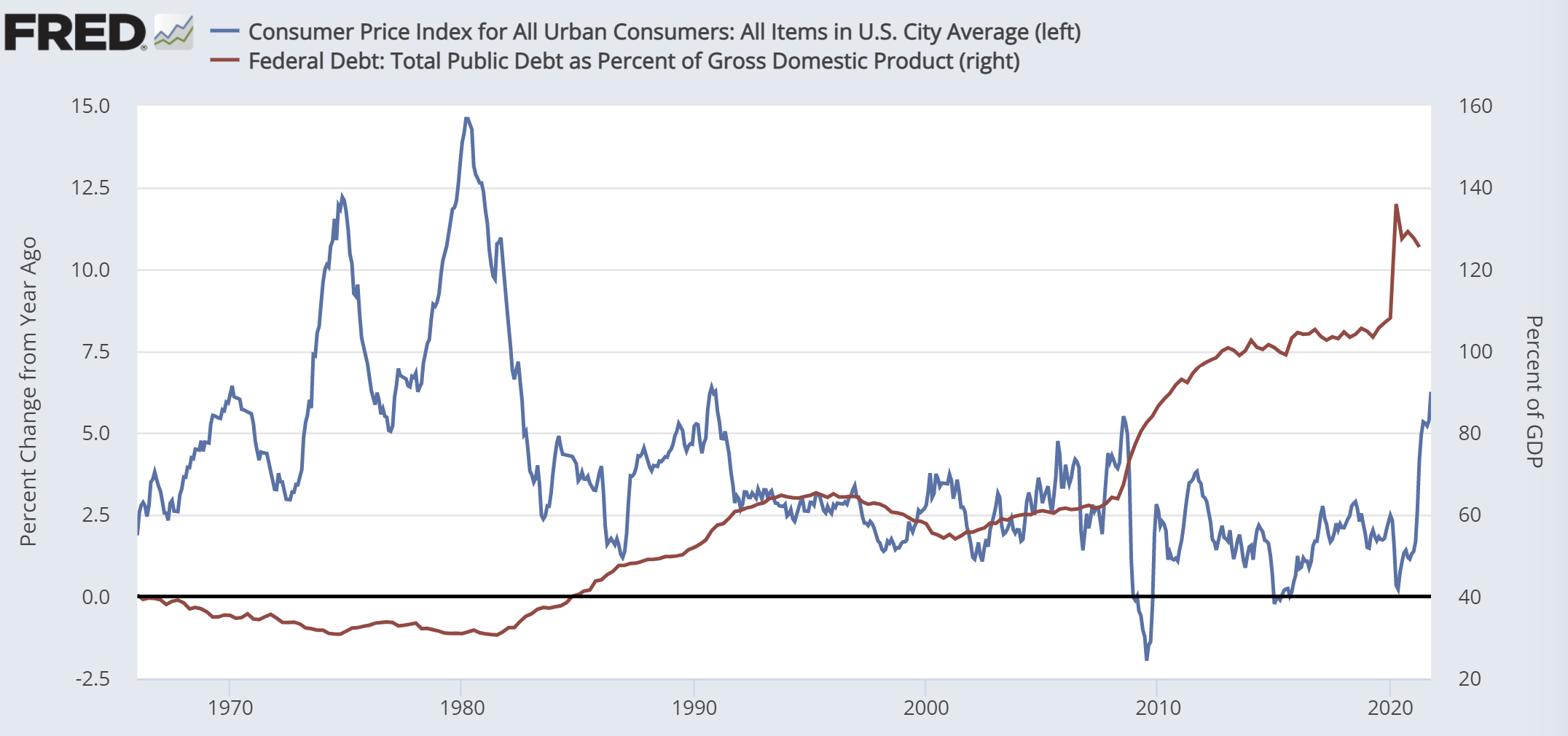

The graph above shows the US debt to GDP (red line, scale on the right) at just under 40% in the early 1980s when Volcker was doing his magic. With the current debt to GDP levels at around 125%, the Fed of 2021 simply doesn’t have the ability to hike rates in the same way without potentially raising the cost of debt so high that the US Federal government could be rendered functionally insolvent.

Aggressive rate hiking would therefore hobble the US Federal government. It has been the combination of quantitative easing (QE) by the Fed coupled with aggressive pandemic-related deficit spending by the Federal government that has marked the key change from previous periods of QE. This de facto monetisation of the US deficit is another key departure in terms of the argument for a shift to secular inflation, should it continue. With US deficit spending on climate initiatives, infrastructure, and arguably entitlements likely to continue or grow, then the Fed’s room for manoeuvre is strictly limited. While a tapering of QE has been announced, this only really mirrors a reduction in government bond issuance so isn’t really tightening at all, at least not in the context of CPI inflation at 6.2%.

The trap for Jay Powell is that a hiking cycle commensurate with current government debt levels will always be so moderate that it will be chasing inflation rather than taming it a la Volcker. It may prove just enough however to pop some of the many asset bubbles that are currently evident in US markets. This scenario, if left unattended (ie without a swift policy reversal), could lead to a period of outright deflation and the severe economic and social consequences that would entail. The current flattening of the US yield curve (with short-dated yields rising relative to longer-dated ones) also hints that the US economy could be slowing, and that any hiking now would be a policy mistake, even with rampant inflation. The logic here is presumably that rate hikes (to temper demand) would not solve an inflation situation caused by a supply-side issue.

The Fed’s goal thus remains the same - maintaining a narrative of passing inflation to keep bond yields low while also acting as little as possible actually to tighten monetary policy, as any tightening risks not only a recession but a crisis in the capital markets. Not a fun job - perhaps Mr Powell would quite fancy someone else having a stab at it.

The nature of inflation is a changing dynamic , in no small part this is a reflection of the culturally adopted ‘cheaper tomorrow’ behaviour that the internet has created and of course the low rates back drop.

The two functions have been an enabler of corporate financial growth with precious little organic growth / real margin growth , outside the realms of the originators (tech etc ).

Thus we have the apple cart significantly knocked by an input shock , demand shock as well as supply chain issues for corporates wholly driven by ROE and thus vulnerable to anything that threatens wafer thin margins , with little consumer appetite to tolerate price hikes.

The financial markets and the economy are very different animals - financial markets have been sculpted by liquidity more than fundamentals since the CB manipulation of rates, and the subsequent chase for yield.

So where does this leave us - corporates with little tolerance for operational duress, or input shocks , consumers with little appetite to tolerate price hikes and a rates back drop that has the world addicted to liquidity -

As long as the provision of liquidity prevails we limp along to the next crisis with ever expanding balance sheets and financial engineering, if the liquidity provision is challenged the artifice is revealed for what it is

At this juncture in the midst (not the end) of a pandemic , surging demand / supply input shocks - the decision of the central banks becomes more about placating the greater power (hint that ain’t political) and for my 2cents that liquidity provision continues - and whatever inflation maybe it’s certainly NOT transient , it’s now cultural - and as such financial mkts will continue to discount and ignore the real economy for as long as the greater power (liquidity) remains in control.

Or else redefine the CPI baskets and inflation metrics to suit the convenient political narratives of the day , hour , soundbite.