Inflation and the Crossover Point. A Narrative Lesson from Vietnam.

Inflation and the Crossover Point. A Narrative Lesson from Vietnam.

On the 30th January 1968, North Vietnamese Army (NVA) and Viet Cong soldiers launched surprise attacks on multiple targets in South Vietnam in what was supposed to be a ceasefire during the Tet lunar new year. Tactically it was a disaster for the NVA, with an estimated 45,000 soldiers killed and more wounded. Yet strategically it marked a turning point in the war because it exposed the US government’s narrative as totally false, and American attitudes to the conflict started to change dramatically. Can any parallels be drawn between this story and the inflation narrative of 2021-’2?

War is generally a real-estate business - seize territory from the enemy and hold it. The Vietnam war was different, as it was in part a guerrilla war fought in the South of the country. Territory was fought over but not occupied, robbing the US of any tangible signs of progress. To find a way of quantifying US success, defence secretary and statistical fetishist Robert McNamara adopted the idea of a ‘body-count’ and the ratio of enemy combatants killed to US servicemen lost.

This was clearly madness from the start: not only did the US public care more about the one lost US soldier than the ten dead NVA or Viet Cong, but counting success in terms of bodies was a morally-warped approach that meant any dead body could be counted as a combatant, especially in a guerrilla war. This grossly elevated the risk to the civilian population of Vietnam.

The final measure of the body-count was the ‘crossover point’. This was the point at which the US government claimed that its forces in Vietnam were killing more enemy combatants than could be replaced, and this was what defined winning. By this measure (or what the officials stats said were the measure), the US was well on the way to winning in early 1968. Then came the Tet offensive, where out of the blue the enemy fielded 100,000 troops and could even attack the US embassy in Saigon. Clearly the crossover point hadn’t been reached, even though the US government had said it had been. Despite successfully repulsing the NVA and VC attacks, it looked like the US was losing the war, and this was a terrible shock. The narrative had been a lie.

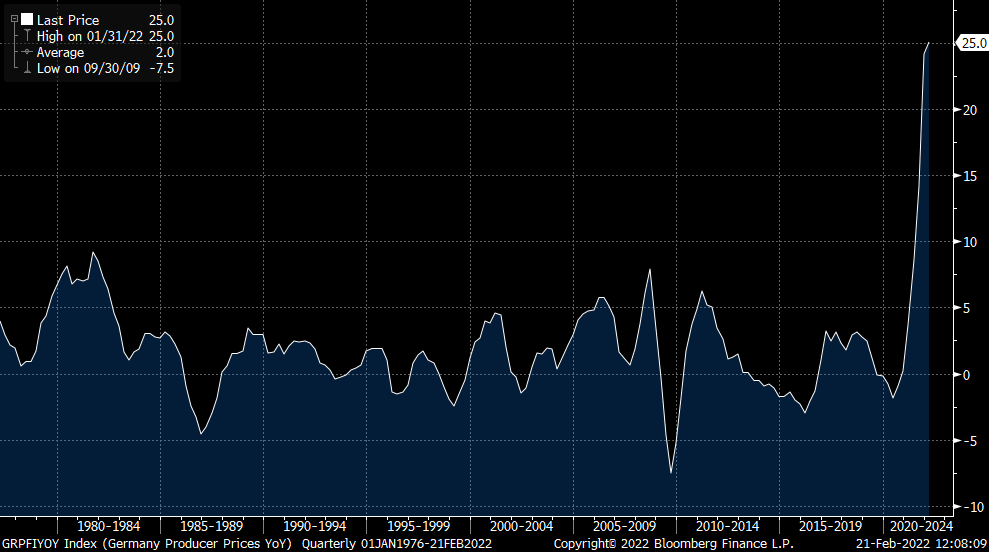

Fast forward to today, and there is a similar problem with the official inflation narrative across the globe, and the claim it was transitory when it wasn’t is the equivalent to claiming you are winning a war which you are really losing. With January CPI inflation coming in at 7.5%, the US is the obvious example, but good old deflationary Europe is struggling too. The graph below shows the producer price index (PPI) hitting 25% for Germany in January 2022 (yes that is 2022 not 1922 when Weimar Germany erupted into hyperinflation). Even excluding headline energy effects, the core PPI registered a staggering 12% year-on-year rise.

Despite this, President of the ECB Christine Lagarde is still talking down the prospect of rate hikes (from negative levels!) in 2022. While much has been made of the recent ECB ‘hawkish pivot’, the facts are that the ECB is still thrashing quantitative easing (QE) and still has negative rates even as inflation reaches a generational high. With typical European alacrity, the EU-level pandemic fiscal spending (decided in 2020) is about to kick-in in 2022 and 2023, providing more stimulus to an already tricky inflationary situation.

Over in the US, much has been made of the rapid flattening of the yield curve as a sign that the US risks recession should the Fed tighten monetary policy too much. By some highly technical measures (the 5yr/30yr overnight index swap or OIS curve), the yield curve has already inverted. Yield-curve inversion portends recessions, and recessions are great ways to curb inflation. But it’s not clear if a recession ahead of the 2022 mid-term elections is really top of Joe Biden or the Democrats bucket list. Despite all the interest-rate hikes now priced, the market is not convinced. Even gold, the investment leper-of-the-year 2021, seems to be sniffing out the Fed’s likely inability to tame inflation in the near future.

Aside from the huge German PPI print mentioned above, some of the moves in the commodity market year-to-date seem almost hyperinflationary. Crude is up 20%, natural gas 25%, aluminium is up 16%, nickel up 16%, corn is up 10%, soybeans up 20% and it’s only February! With the cost of living sky-rocketing, central banks are already starting to worry about wage inflation as the next phase of the problem: governor of the Bank of England Andrew Bailey was castigated for suggesting workers shouldn’t ask for wage hikes despite inflation. Meanwhile on the other side of the pond, President Biden then announced a 4.6% pay increase for Federal workers from 2022 onwards. Some might say this is how price-wage spirals start to spiral.

There is still a sense of unreality about financial markets. While JP Morgan is the latest bank to come out with a new Fed rate-hike estimate (nine-in-a-row apparently), the equity and credit markets, while choppy, are still behaving as though the Fed will come in with another bailout as soon as things look rough. If they do, then one would expect to see a severe hit to the dollar, especially against commodities like oil, gold and copper, and one which will only fire up inflation more. Yet in part, the markets are still acting as though the transitory inflation argument is the proper one, even though it has clearly been discredited. 5y5y US inflation swaps (5yr inflation in 5yrs time) have fallen all of about 20 basis points year-to-date to 2.35% at the time of writing. There is still nothing to see here.

With commodity prices rising sharply, wages starting to shift higher although not yet necessarily ahead of the rate of inflation, price controls on energy becoming an increasingly frequent headline, we may be reaching the point at which inflation is becoming ‘an’ inflation - if you add the indefinite article, it becomes a thing which has a life of its own. After forty years of disinflation, this is quite a shift of mindset, and this may be why the market is taking its time to adjust. When the rising cost of living starts to create political pressure towards wage rises and price controls, that’ll be the point at which some more dramatic repricing may happen in the market.

You can kill inflation stone dead if you mean it. Back in the early 1980s, then Fed Chair Paul Volcker did this by raising the Fed Funds rate to 20%. This followed a decade of the Fed not going ‘all in’ on inflation fighting. By getting the narrative wrong, the danger is that the type of inflationary event we are witnessing now and over the coming years will be worse, with the transitory narrative being the equivalent of the crossover point in Vietnam. When the psychology of inflation changes, you can be losing even when you were winning, just like the US in Vietnam in 1968.

On February 7th 1968, in the aftermath of the Tet offensive, an unnamed US Major was quoted by the Associated Press as saying of the town of Ben Tre in South Vietnam, “it became necessary to destroy the town to save it”. In the crazy logic of the Vietnam War, killing all the civilians was ok if it also meant killing all the Viet Cong. If the Fed did a proper Volcker now and gave inflation both barrels, there is a strong chance the markets and economy would collapse since the overall stock of debt is much higher now than it was in the early 1980s. The real danger though is that we get a few easier inflation prints and then everyone (including the Fed) sounds the all clear. If the inflation mindset is starting to take hold, then the process of fighting inflation will be a long one not a short one - and no one likes a long war.