Europe: is Macraghi the new Merkozy?

Europe: is Macraghi the new Merkozy?

Whether it’s President Biden accidentally saying Russia can invade the Ukraine a little bit or the Fed’s talking heads tanking the stock market by engaging in a bit of competitive hawkishness, the US always seems to hog the headlines. In the background though, Europe is having its own fun and games, and this shouldn’t be ignored.

Europe has an inflation problem, and because the European Central Bank (ECB) is a supranational organisation, the problem is even more political than in the US. Before Christmas, ECB President Christine Lagarde thought it would be nice to call inflation ‘a hump’. It appears nothing has been lost in translation - this is the same transitory argument the Fed was using but which it has since dumped because it was false.

This particular hump appears to be more sticky than anticipated, if humps can be sticky. On the 13th January, ECB vice-chairman and fifth-wheel-in-chief Luis de Guindos was quoted on the wires as saying ‘perhaps inflation won’t be as transitory as forecast only some months ago'. Annual headline inflation in Europe clocked 5% for 2021 with core inflation coming in at 2.6%, significantly above the ECB’s own 2% medium-term target.

25.9% of the increase in headline inflation in 2021 came from energy costs. This is clearly hurting Europe’s industrial base, and since European energy prices, particularly natural gas, remain elevated, the inflationary pressures are likely to persist for at least a few quarters yet.

Back in the 1990s, there was an argument which asserted that if Europe’s economies were perfectly aligned, there would be no need for a single currency, and that if they weren’t aligned, a single currency would fail because of its one-size-fits-all nature, especially with respect to interest rates. The counter argument, pushed by europhiles, was that a single currency could be used as a tool to encourage (force) convergence between the participating economies. This had never been tried before, so the euro as a project is in some senses unique. It also makes it an ongoing, real-time experiment.

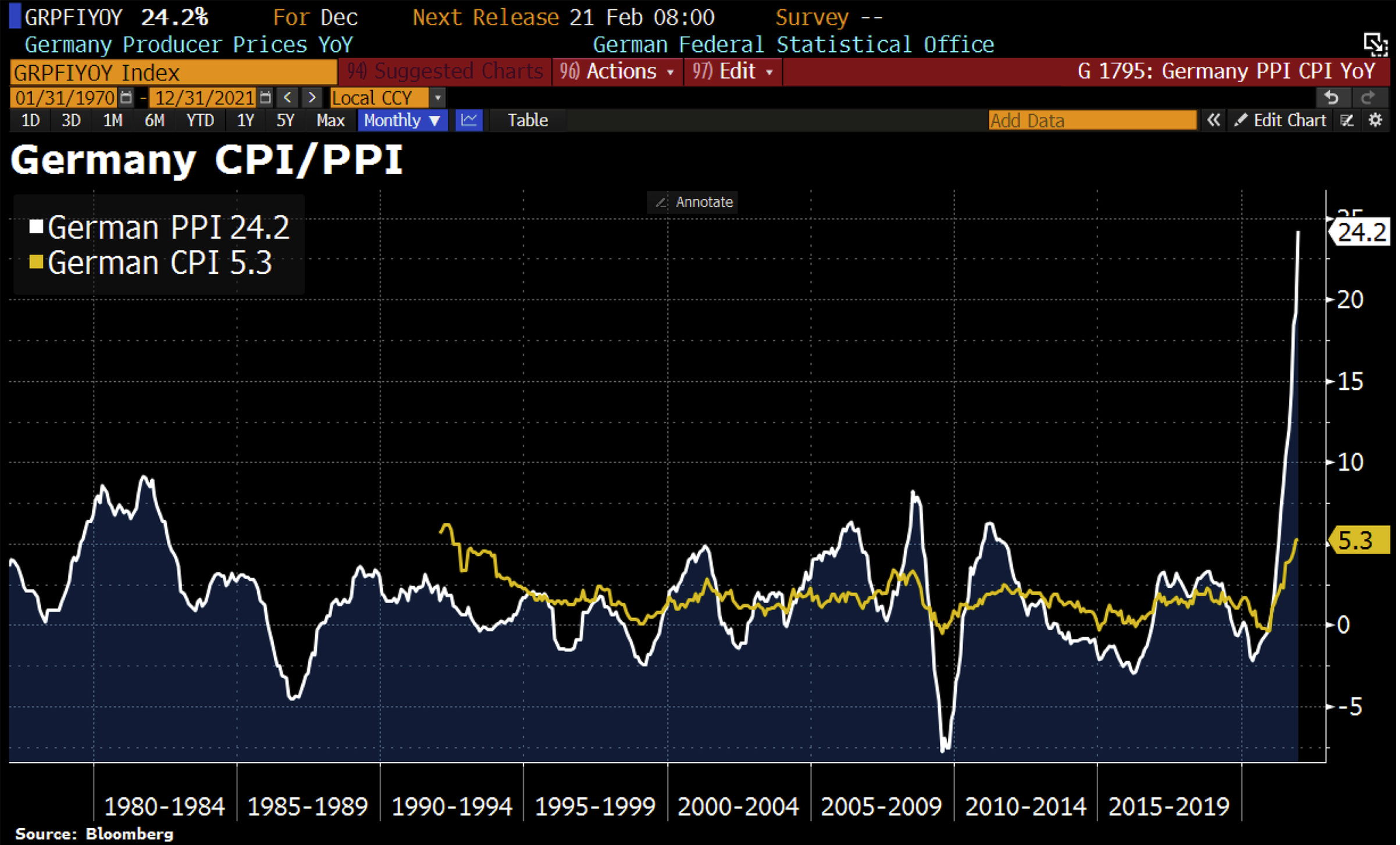

German headline inflation printed 5.3% in December 2021. The last occasion on which the country experienced inflation this high was in 1992, at which time the Bundesbank, which in those pre-ECB days set interest rates, had its discount rate at 8.25%. The current interest rate on the ECB’s deposit facility is -0.5%. The yield on the 10yr bund is currently hovering around 0%, meaning investors in that particular instrument suffered a real loss in excess of 5% last year.

These high levels of inflation suggest that Euro-area interest rates are too low for Germany. The prices being paid by German industry (the purchaser price index or PPI) which tend to lead consumer price inflation (CPI) tend to suggest that this particular hump may have legs, as Sr de Guindos has correctly pointed out. The extent of the problem can be seen in the graph below where German PPI is the white line and CPI the yellow one. PPI at 24.2% is a staggeringly-high figure.

Mme Lagarde has however been vociferous in her assertion that there will be no ECB interest-rate rises in 2022. There is also a debate about whether there will be a cessation of additional quantitative easing (QE) from the pandemic emergency purchase programme (PEPP) when it expires this March. Predictably, it is the Germans, Austrians and Dutch who are pushing for reduced ECB bond purchases.

The problem for the ECB is the outstanding stock of debt. Italy’s debt-to-GDP hit 155.8% in 2020. The yield on 10yr Italian government debt (BTPS) is currently around 1.27%, up nearly 60 basis points in a year. While this is way short of the levels reached in 2012 during the eurozone crisis, the market is nonetheless hyper-sensitive to ECB support for Italy’s bond market - the mere suggestion that the ECB wouldn’t help back in February 2020 saw an instant and large drop in Italian bond prices. Lingering doubts about the solvency of the Italian state means that the ECB needs to be in the market to maintain any semblance of normality, regardless of inflation.

If only this were the whole story. Former ECB President Mario Draghi became the Italian prime minister in January 2021, and his policy was to borrow and spend Italy back to health. Sig Draghi is a sly old dog. Back in 2019 as he was about to leave the ECB, he delivered a speech at Sintra in Portugal promising more QE. This was a unilateral declaration, not discussed in committee with the rest of the ECB board. With market expectations raised, the ECB was bounced into supporting him for fear of a market crash. Similarly, his borrow-and-spend policy in 2021 under the blanket of freedom provided by the ECB’s generous pandemic provisions was a move which effectively dared Germany and chums to demur, something which would risk a crash in the euro and the bond market. So far, he appears to have got away with it.

But wait, that’s not all. Mario Draghi has found a spendthrift buddy in French President Emmanuel Macron, who in turn is keen to splash the cash with a presidential election coming up in April of this year. In an op-ed in the Financial Times (‘The EU’s fiscal rules must be reformed’, FT, 23/12/2021), they jointly outlined a plan to allow more fiscal ‘room for manoeuvre’ and to build on the shared debt issuance principles instituted in the pandemic-related Next Generation EU programme. This policy would be spearheaded by France during its ongoing presidency of the EU. This amounts to a doubling-down on fiscal stimulus at a time of record levels of inflation in the Eurozone. Sturm und Drang!

So while the Eurozone crisis was characterised by the Berlin-Paris axis of Angela Merkel and Nicolas Sarkozy, the push for what the Germans might disparagingly call a further transfer union appears to be a Paris-Rome affair. Macraghi is the new Merkozy, or at least for now - Sig Draghi may well end up as Italy’s new President in a few months, although this need not in theory end his influence at a higher European policy level.

The American economic psyche is one whose formative event was the great depression of the 1930s. Germany’s economic psyche is haunted by the inflations of the 1920s and the post-war era. Thus a situation of rampant inflation, driven by a trifecta of fiscal and monetary largesse, supply-side constraints, and appallingly short-sighted energy policies is particularly worrying for the Germans, especially given the backdrop of France and Italy pushing for what might appear in time to be a new latin monetary union, albeit one funded by the austere, northern-European member states. Mme Lagarde must really be hoping it’s a brief hump.