Does It Really Matter Who Runs the Fed Now?

Does It Really Matter Who Runs the Fed Now?

To say the French armed forces underperformed in 1940 is a bit of an understatement. Strategically out-thought by the Germans and tactically inflexible in their defensive manoeuvers, the French also lacked the resolve they showed in the Great War. This is not supposed to be a slur on the French; quite the opposite in fact. Anyone who has visited the ossuary memorial at Verdun, the site of the great Franco-German slaughter of 1916, will be immediately disavowed of any doubts about the valour of the French fighting man. The memory of Verdun, the mill on the Meuse, weighed heavily in French memories in 1940, and in part explains the lack of tenacity they showed in the field that summer.

In May 1940, with German armour already over the Meuse river, the 68 year-old head of the French army, Maurice Gamelin, was replaced by the 73 year-old Maxime Weygand in a desperate attempt to stem the Wehrmacht’s advance. Without needing to go into detail, the fact the French sought an armistice about a month later on the 22nd June tells us most of what we need to know about the effectiveness of this personnel change.

With reference to the Fed in 2021, especially in the context of imminent news about who will be the next Chair of the Federal Reserve, this somewhat oblique historical example raises two questions - first, the role of individuals in a crisis and secondly, and consequent to this, whether wider economic factors (such as inflation, deficit financing and the national debt) should in fact be the focus rather than a tabloidesque obsession with personality and the individual.

Jay Powell’s current term as Chairman of the Federal Reserve can broadly be divided into two parts; the ‘hawkish’ period up until the end of 2018 and the ‘dovish’ period from 2019 onwards, the latter which obviously includes the monetary response to the pandemic. Mr Powell’s hawkish phase ended with a pivot in January 2019 following a tumultuous end to 2018 in which the credit market effectively closed to new issuance and in which the stock market tumbled around 20% in December. In 2019, prior to the pandemic, he oversaw rate cuts, the reintroduction of quantitative easing (QE) and the introduction of a new Fed repo facility to provide liquidity to the money markets. All of this happened with unemployment at historic lows, the stock market at historic highs, and the US Federal government running a large primary deficit during a period of robust economic growth.

Clearly this volte-face from Jay Powell tells us a lot about the importance of the will of the individual with respect to the wider macro forces affecting interest rates and growth in the US economy. From being on the front foot with respect to rate hikes, Mr Powell was forced by the market to pivot sharply. The advent of the pandemic, especially with respect to deficit-funded furlough payments for workers, forced the Fed into a de facto monetisation of the US deficit. Added to this, the growing political pressure with respect to the energy transition from fossil fuels appears to be setting the scene for a new phase of fiscal intervention which will most likely demand the involvement of central banks in terms of capping bond yields to keep the cost of the green revolution manageable. The overall direction of travel seems clear.

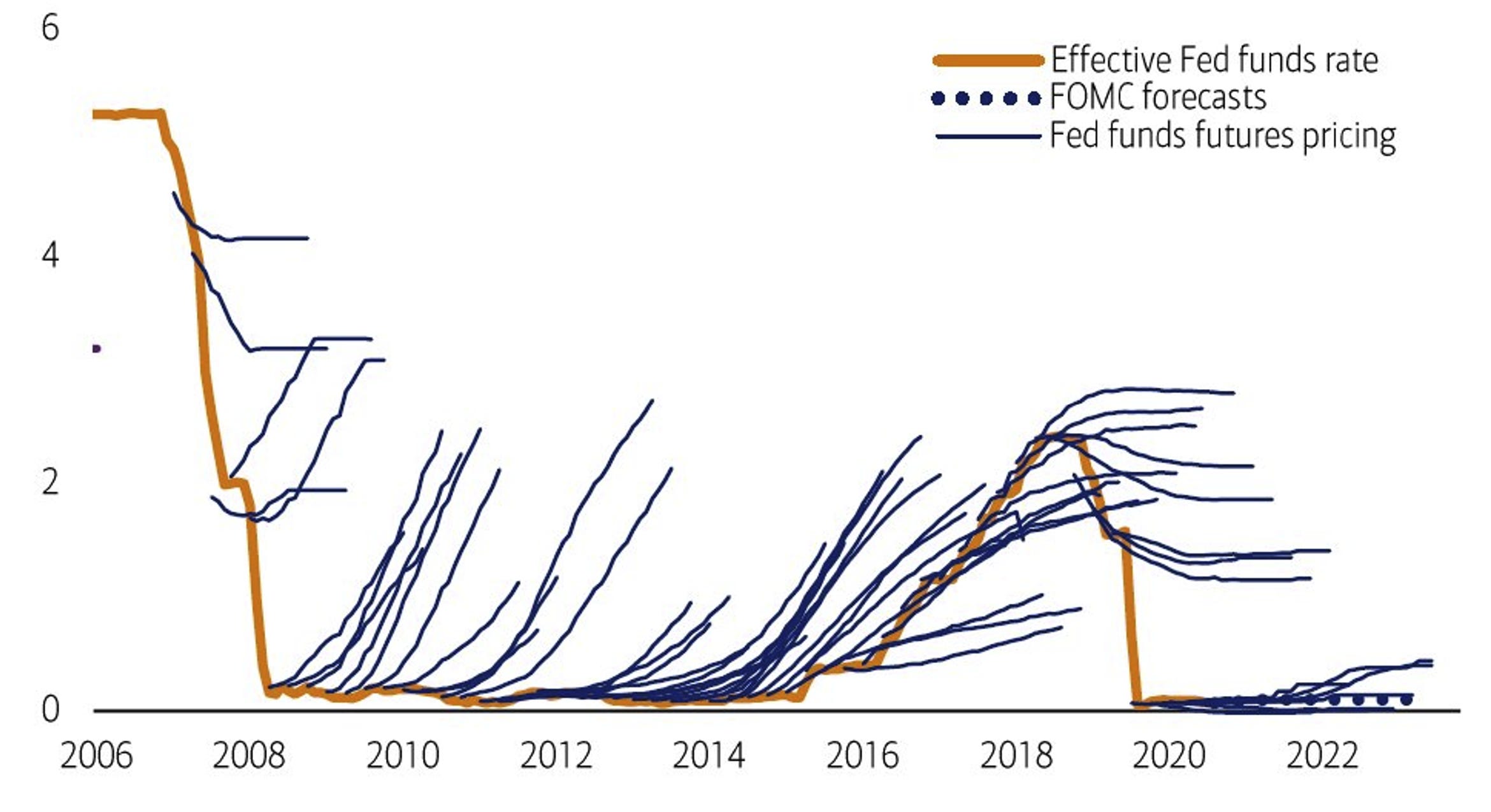

Yet the scope of possible Fed monetary policy in the next few years ought to be considered as much in the context of its activity prior to the pandemic as it should do with respect to the currently pressing issue of strongly-rising inflation. The introduction this summer of a standing repo facility (SRF) for domestic needs and a permanent repo programme for foreign dollar borrowers ought to help should there be another crisis in the outwardly-boring but critical dollar repo market similar to the one which happened in September 2019. It is however with interest rates - the Fed Funds rate - where the market is currently preoccupied, largely because the Fed appears to be very much chasing the game with respect to inflation.

The graph above, courtesy of BofA research, shows an interesting history of Fed Fund futures. These futures, which reflect the anticipated future level of the Fed Funds rate, are currently pricing a first rate hike in mid-2022 and potentially others later in the year. This historical graph can be read a number of ways. It provides a strong argument for the transitory-inflation camp in that the market constantly priced in high inflation after the start of the first QE programme in December 2008 which never actually materialised. The idea behind this is that QE only affected financial assets (raising bond prices and the stock market) rather than spilling out into the real economy. On the other hand, this graph could be interpreted as reflecting a general willingness of the Fed to maintain loose monetary conditions but an institutional bias against tightening, despite market expectations.

Back in 1994, James Carville, political advisor to Bill Clinton, famously said that if there were such a thing is reincarnation, he would like to come back as the US bond market in order to scare people. It is here in the bond market, especially with respect to the stock of debt, that focus should be. US debt-to-GDP is currently around 125%. The Federal government is still running a substantial deficit, albeit a smaller one than last year.

The bond market is the limiting factor for the Federal Open Market Committee (FOMC) with respect to rate hikes in the coming year or so. Regardless of whether one believes that inflation is transitory due to a supply-side shock from Covid-19 or increasingly secular due to a deficit-monetisation which marks a change from previous episodes of QE, the message from the bond market is increasingly clear. Even if Fed fund futures are pricing in swifter rate hikes, the flattening of the yield curve, where short-dated yields are rising relative to longer-dated ones, suggests that the economy may be slowing and that aggressive action from the Fed might end up constituting a policy mistake. Thinking a step ahead, it’s not so much the end of QE or the first rate hike which matters, but the actions which the Fed will have to take to reverse a possible policy error.

The Fed has a dual mandate of employment and price stability. If it leans to the former (a stance which would be popular in the White House), it will likely remain very dovish. The Fed’s talking heads are however already mentioning a faster-than-expected taper of QE, which suggests the market is pressuring them into a less dovish stance. In any case, this isn’t really hawkish in any historical sense. The last really hawkish thing the Fed did was hiking rates between meetings in July 1994 - if they did this now, it’s likely you’d have a market meltdown. Back in 1994, this hawkish move caused a major bond-market crisis, and this was when the national debt was a third of its current size.

Jay Powell says the Fed has the tools to fight inflation. Like the French and the memory of Verdun, the Fed is relying on the memory of the late Paul Volcker and his assault on inflation in the early 1980s. Yet even Mr Volcker said that a repeat of his policy stance would now be impossible due to the size of the national debt. On the subject of personality, Volcker’s autobiography ‘Keeping At It’ reveals an old-fashioned public servant who was willing to take on the wrath of politicians, the public (and the market) because he felt the ends justified the means. In the light of the recent trading scandals at the Fed, one wonders whether the current crop of personnel are really made of the ‘right stuff’ needed in an inflationary crisis - particularly if this meant defying Wall Street and the White House simultaneously.

This puts into context the current speculation about whether Lael Brainard will be nominated to replace Jay Powell as the new Fed Chair. Subject to her approval by Congress, the market anticipates that Ms Brainard would be a dovish candidate, compliant with White House spending plans. Those plans have of course to be taken in the perspective of the upcoming mid-term elections in 2022 where the Democrats risk losing control of at least the House of Representatives. More immediately, the market may pass its judgement on Brainard as Fed Chair through a weakening of the dollar.

That might be the price to be paid for a Fed seemingly in tune with White House plans, but ultimately it will be the US bond market which decides what level of yields would be commensurate with a Fed Chair who was even more dovish than the incumbent. Not necessarily bond vigilante stuff, but nonetheless a major steer for Fed policy, especially with the tapering of QE reducing its day-to-day control over Treasury yields. Perhaps it’s the national debt that runs the Fed these days.