Are we about to see a Ratners moment in the FX markets?

Are we about to see a Ratners moment in the FX markets?

As far as business self-immolation goes, no story is quite as good as the Gerald Ratner one. The inheritor of a high-street jewellery chain who had until that point barely put a foot wrong, Mr Ratner managed to torpedo his own company in the most impressive style when making a key-note speech at the Institute of Directors in 1991. With a rhetorical flourish, he asked himself, “How can you sell this [jewellery] for such a low price?” He answered his own question by saying, “because it’s total crap.”

Cue a share price collapse, a desperate rebrand from Ratner’s to Signet Group, but all to no avail. The damage was done, and Ratner secured himself a spot in business infamy.

Since the 1990s, central banks in the developed world have targeted an average annual rate of inflation of 2%. Following the largesse of the lockdown-driven deficit spending of 2020, the subsequent Covid-related supply-chain disruptions and now the emerging economic catastrophe of anti-Russian sanctions, global inflation has shifted gears. The 2% target which central banks could scarcely manage in the decade after the global financial crisis now seems to be firmly in the rear-view mirror, and it looks like there is a bit of a problem.

The problem is the need to hike rates to fight inflation to the backdrop of a massive outstanding stock of debt.

The Bank of England has hiked twice, and the Fed once, although the market is now pricing in as many as 8 or 9 further 0.25% Fed hikes in 2022, including a 0.50% hike at the upcoming Federal Open Market Committee (FOMC) meeting in May. In the light of Russia’s apparent pegging of its currency to oil and gas, there has been a lot of chatter about the decline of the dollar as a reserve currency, but it is really the decline in some of the other developed-market currencies which stands out right now.

Since the start of the year, the euro has declined from around 1.14 against the dollar to around 1.08. More spectacularly, the Japanese yen has fallen from 115 to 125 against the dollar (see graph below). Both the European Central Bank (ECB) and the Bank of Japan (BoJ) have something in common; despite both currency areas generally running current-account surpluses (more money flowing in from trade than flowing out on a net basis), the apparent unwillingness of these central banks to implement rate hikes is starting to spook the market.

Japan and the Euro area are both heavy energy importers, and clearly the spike in oil and especially gas prices is driving inflation expectations higher. In Japan’s case, this has started to affect its balance of payments adversely. The relative weakness of the yen and the euro against the US dollar since the start of March sits in stark contrast to the strengthening of the currencies of a number of commodity-exporting countries against the dollar over the same period, most notably the Brazilian real, the Aussie dollar and the South African rand.

The BoJ has announced that it wants to try to keep yields on the 10yr JGB (Japanese Government Bond) at 0.25%, and it seems that the ECB might be working on a similar plan. A Bloomberg article from the 8th April (‘ECB is crafting a crisis tool to activate if bond yields jump’) mentions that some ‘instrument’ is being prepared, but as yet there are no firm details. Whatever it is eventually called, it will likely involve buying euro-area bonds in order to offset any adverse rise in yields.

Central banks can control either the cost of money (through interest rates) or the amount of money (through the discounting of bills or through policies such as quantitative easing), but not both. The large stock of debt in Japan and the Euro area (especially in the Club Med countries) suggests that an economic crisis may become a reality if bond yields were to rise too far. This is true not only in terms of a crisis for government finances but also in Europe as a potential bank solvency issue, since euro-area bank-reserve capital is largely made up of government bonds from their own country of incorporation.

With the BoJ having effectively announced yield-curve control, and with the ECB clearly toying with the idea, it seems that a focus on the cost of money will mean an increase in its stock, hence the fall in the yen and the euro against the dollar. To add more fuel to the inflationary fire, the anti-Russian sanctions are starting to make their effect felt on the countries implementing them.

In Europe, Italy’s PM Mario Draghi is calling for an EU-wide price cap on gas as a means of tightening sanctions on Russia (Il Corriere, 18/04/2022). In reality, this is a push for more deficit financing to keep domestic energy prices from rising further. Further sanctions, or even an outright boycott of Russian energy exports will cause more price rises as well as a possible economic crisis for households and businesses which will likely necessitate government and central bank intervention. If energy subsidies such as the ones Sig. Draghi is calling for are implemented, the direction of travel for the euro is clear. You can print money, but you can’t print energy.

What about the dollar? in a recent article in the Financial Times, Scott Minerd, the CIO of Guggenheim Partners, suggested that the Fed may well try to control the amount of credit in the US economy (rather than interest rates) as a means of slowing the economy, albeit at the risk of a nasty recession given the large stock of government and corporate debt (‘For lessons on fighting inflation, skip Volcker and go to 1946’, FT, 21/03/2022). Certainly the Fed’s stated desire to reduce the size of its balance sheet by letting maturing bonds run off (quantitative tightening or QT) suggests that this at least is the plan.

In a letter in response to Mr Minerd’s article published in the Financial Times (whoop), I pointed out that from 1942 to 1951, the Fed in fact implemented a strict policy of yield-curve control of its own, and that the pegging of rates during that period of high inflation greatly reduced the real value of the US debts which had been incurred due to World War II (link - FT letters 23/03/2022). Back then the dollar held up, and while it may still hold up against currencies such as the yen or the euro if only because the US is more energy self-sufficient, pressure may appear elsewhere.

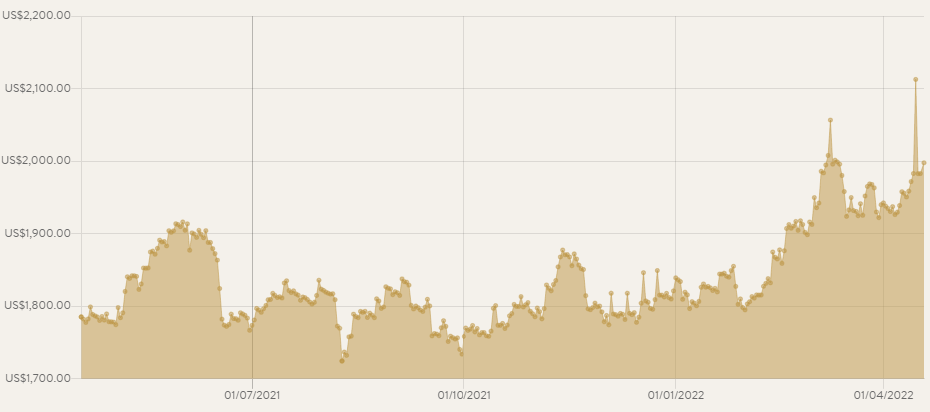

How is it possible to tell the market is sniffing out the possibility of Fed yield-curve control or at least the possibility of a dovish pivot? While the euro and yen are sliding against the dollar, gold is holding up surprisingly well against the dollar in the face of the rate-hike fever which is currently gripping markets (see graph below). While the euro-dollar futures market is actually starting to price in Fed rate cuts further out, it is arguable that gold is also telling us that any rate hikes the Fed is able to implement may not be enough to tame inflation, or that the treasury bond market may start to struggle before the desired neutral level of interest rates is reached.

What the stickiness of the gold price indicates is that the reality of a highly-indebted US government means that the Fed is constrained in its rate hikes, and if there is a policy mistake in terms of raising interest rates to a point at which the bond market, the credit market, the stock market and/or the economy (or all of them) start to crack, then it is likely the Fed will have to pivot back to a more-accommodative policy stance even before the inflation dragon is decisively slain.

While the name for the central bank policy instruments may be different this time, they’ll likely be just another incarnation of quantitative easing, possibly with more-explicit yield targets. This time there may even be moves towards capital controls or at least policies which start to herd domestic investors into bonds by some regulatory means in order to create demand for government debt instruments. If inflation proves persistent, this is very bad for bond holders - unlike Ratners, governments have the ability to make people buy even if the product is rubbish.

If you enjoyed this post, please click subscribe below to get the next instalment sent direct to your inbox. It’s so cheap it’s free.