A good recession will put an end to inflation, right?

A good recession will put an end to inflation, right?

One of the theories of history which is unsurprisingly less popular these days is the ‘great man’ approach. The high priest of this type of analysis was the nineteenth-century historian Thomas Carlyle, whose 1840 work, “On Heroes, Hero-worship, & The Heroic in History” generally does what it says on the tin. The idea that “Great Men should rule and others should revere them” doesn’t really seem to jive with the inclusivity and diversity message which is currently en vogue.

For the US Federal Reserve, Chairman Jay Powell is trying to channel the spirit of his late predecessor Paul Volcker who history remembers as the monetary hero who tamed inflation by raising the Fed Funds rate to 20% in 1981. The Fed Funds rate is currently at 2.5% while US June CPI inflation wa s 9.1%, a fraction lower than the peak levels of the early 1980s.

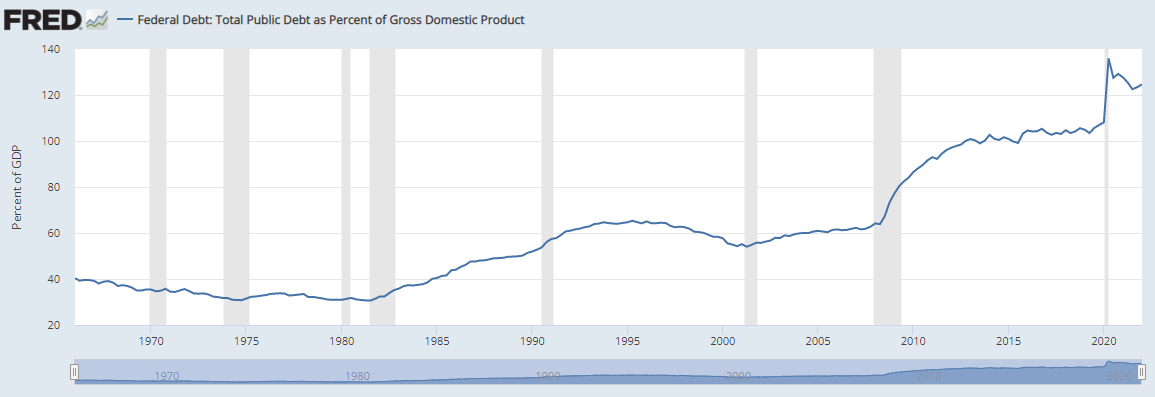

There are a number of reasons to believe that the Fed’s Volcker-worship is nostalgic rather than realistic. Before his death in 2019, Paul Volcker himself said his actions in the 1980s would be impossible to repeat because the stock of debt had grown so much in the intervening four decades. The graph below illustrates his point in terms of the US national debt - just over 30% in 1980 and well over 120% at the start of 2022.

With the current Fed Funds rate at 2.5% and CPI inflation at 9.1%, the real Fed Funds rate is -6.6%. In 1981, the Volcker hikes took this real rate to positive double digits. This was an inflation-crusher, but the price paid was a deep recession with unemployment peaking at 10.1%. The 1981-2 recession retained the moniker ‘the great recession’ until the 2008 one.

The last time the Fed took rates above the current (yet historically-modest) level of 2.5% was in 2018, and during the second half of that year, the US stock market collapsed and the credit market effectively closed. This is what Mr Volcker meant by saying the stock of debt was a limiting factor to aggressive rate hikes.

Even if the Fed wants a deep recession to tame inflation, it may precipitate a financial crisis which necessitates a central-bank policy reversal well before it achieves the permanent demand destruction which that sort of deep recession normally causes. This is separate from any political considerations relating to what a high level of unemployment would do given the upcoming US mid-term elections and the 2024 presidential contest. Successfully navigating the Scylla of permanently-high inflation and the Charibdis of a debt-deflationary trap would certainly warrant a Homeric level of adulation for Jay Powell.

Homer’s Odyssey was a myth. The problem with hero stories is they tend to be stylised and simplified. There were a number of other things going on in countries like the US and the UK during the early 1980s which can explain the taming of inflation. Part of the wage-price spiral which was a feature of the inflationary surge in the 1970s was the role of organised labour (unions) in demanding better pay and conditions. Events like President Ronald Reagan’s sacking of over 11,000 striking air-traffic controllers in 1981 and UK Prime Minister Margaret Thatcher’s long-running battle with the miners that reached a hiatus in the mid-1980s are as much a part of the story of the curbing of inflation as Volcker’s rate hikes.

The other hero-free part of the 1980s inflation-taming story is how business adapted. A combination of changing operating practice to increase efficiency together with capital expenditure increasing production capacity eventually moderated price increases, especially in the energy industry. The 1973 oil shock had been a key event in the 1970s inflation story; the emergence of the North Sea as a new and less politically-sensitive source of gas and oil ought to be considered as an example of the long battle against rising prices in which capitalism itself did as much as great men to turn things around.

In a similar spirit to which North Sea gas was a saviour for the UK in the late 1970s, so it seems oil discoveries off the Falkland Islands in the South Atlantic might be an answer to the UK’s current energy crisis. The exploration company Rockhopper (a rockhopper is a type of penguin for the uninitiated) appears to have found a tasty 500 million barrels or so of oil in the Sea Lion field (‘Falklands black gold rush might finally be a reality’, The Times, 23/07/2022).

This discovery is perhaps enough to fill a Putin-sized gap in the UK’s energy requirements, irrespective of what Argentina and Sean Penn say. When it comes to commodity-price inflation, higher prices are eventually the cure for higher prices, but the process of committing capital for exploration and plant is a slow one, made more tortuous in recent years by the environmental movement making pariahs of the oil industry. A key measure of the supply-side story of inflation moderation will be monitoring the relative preference of the oil majors in favouring dividend payments and stock buy-backs over capex. Only an emphasis on the latter will mark a key shift in the long-term inflation story for energy in the developed world.

So while the market is focusing on monetary factors like central bank rate hikes and balance sheet reduction, a long-term view of inflation ought also to contain a sober look at wage inflation and also the investment cycle with respect to commodities, especially for energy and energy-related infrastructure. If the high global stock of debt means central banks can only cause recessions without actually killing inflation dead, then we may yet see a return to a boom-bust cycle (or stop-start cycle as it was known in the 1970s) which may disrupt the corporate investment cycle thereby lengthening the overall inflationary episode.

Some progress is clearly being made - nuclear energy is all of a sudden a lot greener than it was last year, with even the Atomkraft-shy German government potentially restarting a number of reactors. But the commodity capex cycle is a long and slow one, and one which this time around has to battle against the environmental movement and its heroes like Greta Thunberg. Recession or not, the struggle to tame inflation may take some time.